Happy New Year 2006

Dear Visitors, I wish all of you a Happy New Year & Happy Emotionless Investing!

Investing is most intelligent when it is most businesslike - Benjamin Graham (1894-1976)

____________________________________________________________________

Value-Stock-Plus stands at No. 50 in the list of Top 100 Finance Blogs by ValueWiki

Recognised by The Economic Times as one of the most popular financial blog

Updated! Compilation on

Warren Buffett,

Rakesh Jhunjhunwala

& Charlie Munger

____________________________________________________________________

Dear Visitors, I wish all of you a Happy New Year & Happy Emotionless Investing!

Click on the link to read the full story

Click on the link to read the full story

Markets: The writing is on the wall!

End of bull run or long-term bet?

Analysts` corner: Hero Honda

Stock watch: Mahindra Ugine

Vivek Paul set to ink deal with Sharekhan

Momentum in auto ancillaries: Morgan Stanley

Brics initiates buy on Petronet

Indian equities expensive: ML

Country funds hot now: Durham

For Finance St, 2005 has been a year to remember

Operators run rings round the Sensex

Reliance demerger: You ain’t seen anything yet - a good read!

How GDP is estimated in India

The incredible power of compounding - a good read too!

"In the short run, the market is a voting machine but in the long run it is a weighing machine." - Benjamin Graham

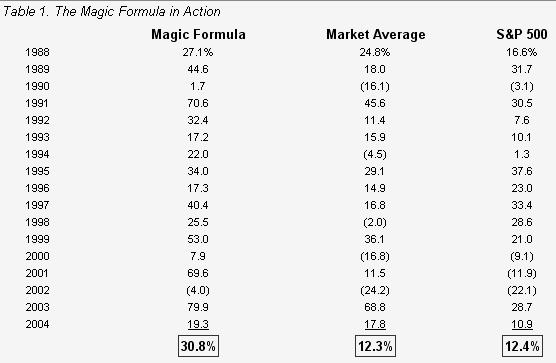

Note: The "market average" return is an equally weighted index of our 3500 stock universe. Each stock in the index contributes equally to the return. The S&P 500 index is a market weighted index of 500 large stocks. Larger stocks (those with the highest market capitalizations) are counted more heavily than smaller stocks.

Over 17 years, earning 30% a year means $11,000 would have turned into over $1 million! Not bad.

But what if we made it even easier for people to follow the magic formula? What if we created a free website--magicformulainvesting.com--that made finding "magic formula" stocks completely automatic? Would that convince you to try it yourself?

Actually, maybe not. With me being such a blabbermouth, if everyone "knows" the "magic formula" maybe it will stop working? After all, how can any strategy keep working if everyone follows it?

Well, here's the answer. The great thing about the "magic formula" is that it isn't that great! It doesn't work all the time. That's right. Over long periods of time, it's true, the results are amazing. But...there are still 1, 2 and even 3 years periods when the formula doesn't work at all! Most people just don't have the patience or the discipline to stick it out during those tough periods. After a year or two of following a strategy that underperforms the market, most people simply give up!

That means for the "magic formula" to work for you, you must "believe" that the formula makes sense and that it will continue to work over the long term--even if it hasn't worked for months or even years. For that, you'll have to understand why the magic formula makes sense. You'll have to continue to believe that it still makes sense even when friends, experts, the news media, and Mr. Market indicate otherwise. That's tough to do! Unfortunately, to really "believe", I mean really, truly "believe", you'll have to be convinced that buying above average companies at below average prices actually makes sense. I believe it does. I hope you "believe" too.

If you do, I know you'll become a more successful investor. But darn if I didn't just give away the ending.

Source: John Mauldin Newsletter

Note: The "market average" return is an equally weighted index of our 3500 stock universe. Each stock in the index contributes equally to the return. The S&P 500 index is a market weighted index of 500 large stocks. Larger stocks (those with the highest market capitalizations) are counted more heavily than smaller stocks.

Over 17 years, earning 30% a year means $11,000 would have turned into over $1 million! Not bad.

But what if we made it even easier for people to follow the magic formula? What if we created a free website--magicformulainvesting.com--that made finding "magic formula" stocks completely automatic? Would that convince you to try it yourself?

Actually, maybe not. With me being such a blabbermouth, if everyone "knows" the "magic formula" maybe it will stop working? After all, how can any strategy keep working if everyone follows it?

Well, here's the answer. The great thing about the "magic formula" is that it isn't that great! It doesn't work all the time. That's right. Over long periods of time, it's true, the results are amazing. But...there are still 1, 2 and even 3 years periods when the formula doesn't work at all! Most people just don't have the patience or the discipline to stick it out during those tough periods. After a year or two of following a strategy that underperforms the market, most people simply give up!

That means for the "magic formula" to work for you, you must "believe" that the formula makes sense and that it will continue to work over the long term--even if it hasn't worked for months or even years. For that, you'll have to understand why the magic formula makes sense. You'll have to continue to believe that it still makes sense even when friends, experts, the news media, and Mr. Market indicate otherwise. That's tough to do! Unfortunately, to really "believe", I mean really, truly "believe", you'll have to be convinced that buying above average companies at below average prices actually makes sense. I believe it does. I hope you "believe" too.

If you do, I know you'll become a more successful investor. But darn if I didn't just give away the ending.

Source: John Mauldin Newsletter Click on the link to read the full story Indian banks to weather storm in volatile 2006 Convenios is the next big retail story Equity allocation in your investment portfolio ‘India is comprehensible to long-term investors’ Analysts' Corner: Everest Kanto Stock watch: Himatsingka Seide What's So Big About a Speculator? - good one! Dos and Don'ts for investors Brics maintains 'buy' on RIL Buy on Rain Calcining: Anand Rathi ML maintains 'buy' on Jet Airways "There are two requirements for success in Wall Street. One, you have to think correctly; and secondly, you have to think independently." - Ben Graham

Click on the link to read the full story

IPO scam...SEBI needs to act quickly

Group of investors acquire over 5 cr shares of Reliance - huh!

Poor governance can stop the bulls

Don't mistake activity for achievement.

| $10 billion FII inflows, Corporate profits at 5 per cent of GDP, 87 companies in the billion dollar club, Sensex at a life-time high, M-cap at $500 billion. |

| Click here for Chart Book 2005 (2.5mb .pdf file) |

Source: Equitymaster.com

As we enter the fifty-second week of 2005, the final one for this year, and when the Indian markets are nearly at their all time highs, there's one phrase that reminds us of the situation prevailing around. It goes like this - "Human nature is human nature and human nature would continue to remain human nature till human nature remains human nature." - (Late) Nani Palkhivala. Now, one would ask why this quote on a website dedicated to equities. Well, this phrase, when used in context of equity investing, holds true to a very high extent.

History is replete with examples when greed and fear (key ingredients of human nature) have taken over discipline, resulting into windfall gains and, of course, 'windfall' losses for investors. And more sadly, small investors are the biggest losers in these phases of indiscipline (recollect the year 2000 stock market boom and bust, or in case of those with short memory, May 17 2004. While greed results into bulls taking the centre-stage and leading markets towards nauseatingly high levels, fear brings them back to ground zero. And small investors suffer in both these situations.

As we are about to enter the year 2006, the second last year of the tenth five-year plan, Indian equity markets are at their all-time highs. While such a situation brings in factors that cause the 'greed' element to rear its face, investors need to practice utmost caution and not give in to temptations that rising markets like these bring with them. This calls for high levels of 'discipline' and, in these times, this should be like a resolution for the New Year.

Now, while making a New Year resolution is quite easy, practicing the same is otherwise. And when that resolution demands high levels of discipline, the task becomes all the more burdensome. First of all, most of us generally fail to make reasonable resolution(s), and that is the major reason why most of us fail to keep the one(s) we make! Sure, all New Year resolutions do not make it past the 2nd of January, but wisdom would be in believing that this year is going to be 'different'. Right? Happy New Year!

Fertilisers: High yield to maturity Overseas offerings: The capital Nirvana `Inflation, interest rates driving gold' Lessons from Yes Bank IPO scam

New features of stock market surge

"Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid." - Warren Buffett

There may be value for patient investors from exposures in select companies with sizeable investments. The ones that make the cut are Tata Investment Corporation, Parry Agro, Ramco Industries, Maharasthra Scooters, Zuari Industries, Rane Holdings, Atul, Indian Oil, Eicher and SRF Polymers. Click Here for the complete article.

Click on the link to read the full story Analyts' Corner: Rajasthan Spinning: Capacity addition boosts Sensex: Crystal gazing In Focus: Carbon credits Asian steel prices to stabilise 2006 Investment Checklist Stock watch: VisualSoft Tech Analyts' Corner: Nagarjuna Const: higher RoE BSEL Infrastructure Realty Ltd. from ICICI Just how big is China’s economy? Insight: Rediff’s second coming; ICICI Bank slips "Some say opportunity knocks only once. That is simply not true. Opportunity knocks all the time, but you have to be ready for it." - Louis L'Amour

The markets continue to hit all-time highs, even as, at every rise, 'market experts' advise caution! As more and more FIIs buy into the India story, wanting to get a piece of the action, valuations keep on moving higher and higher. Consequently, finding value in stocks is becoming increasingly difficult. The large cap stocks seem richly valued at current levels (barring a select few) and it appears that most of the growth in the medium-term has been factored in.

In such heady times, where idea generation becomes more and more scarce and difficult, theme-based investing can make things a little easier for investors. In simple terms, theme-based investing means identifying a particular 'theme' in the country that is likely to become a strong growth story going forward, due to reasons such as increasing demand, favourable policy environment, nascent market to be tapped, and so on.

Examples of theme-based investing abound in the history of the Indian stock markets. Liberalisation, privatization, information technology, commodities and infrastructure are examples of major themes, based upon which the markets rallied in the past, of course, with the help of the FIIs.

This time around, it is the 'emerging markets' theme that has played out and continues to do so. This has actually been the major theme based upon which FIIs have poured in massive sums of money into the Indian stock markets and, for that matter, other emerging markets globally, like Taiwan and Korea. Of course, it must be noted that while this example is from the point of the view of the FIIs, on a retail basis, the theme could be sector specific.

Thus, one needs to first pick the theme that one likes and that one feels can deliver good growth over the medium to long term and then, of course, do the requisite stock picking. We believe that 2 themes have a strong chance of playing out over the next few years - 'domestic consumption' and 'outsourcing'.

Domestic consumption Given India's burgeoning middle class population, favourable demographics and increasing affluence, we believe that sectors that are focused on domestic-led consumption could benefit in future. Sectors that are expected to do well range from FMCG, two-wheelers, consumer durables, tractors, telecom, PCs and retailing. In fact, the rural market is highly untapped and this is undoubtedly where the future growth of India Inc. needs to come from if the country is to reach the next trajectory of growth.

To substantiate this with an example, in the telecom sector, India's cellular teledensity is just around 6.5% to 7%. Therefore, there is significant scope for growth. However, if we break this up between rural and urban areas, urban India's cellular teledensity is 32%, while that of rural India is just 1%! Thus, we believe that it is in the rural markets where the next phase of growth needs to come from, if India is to grow in a sustainable manner over the longer term.

Outsourcing India's attractiveness as an outsourcing destination is only too well known. Just ask techies in the US, UK and Europe! India's pre-eminent position in IT-BPO outsourcing is due to factors such as low labour costs, highly skilled engineering and management talent, enabling policy environment, mastery of the art of global delivery and execution excellence. Therefore, global Fortune 1000 companies and beyond are really looking very seriously at India for outsourcing/offshoring their work.

But while India's software exports story has been known for many years now, we believe that the time has come for India to stand up and be counted as a viable manufacturing destination as well. Of course, we need to ensure that we stick to our strengths. China has strengths in mass manufacturing, while India can carve a niche in higher-end products and design and development of products. Auto ancillaries, pharma and textiles are 3 major areas that have the potential to grow at an impressive pace in future and replicate the success of the software industry.

However... It must be noted that identifying a theme is easier said than done. Markets latch on to 'the next big thing' very quickly and very soon, the theme plays out. Investors must have the foresight to be able to identify themes. But then, the next step is equally important, if not, more so - that of stock picking. Investors in technology stocks were on the right track when they picked the theme (the fact that it turned out to be a huge bubble is another matter). But then, investors who went for stocks like Pentamedia Graphics and DSQ Software would have ended up losing most of their investments. This is because these kind of companies did not have stable and robust business models, unlike Infosys or Wipro, which is why they are still languishing at low stock prices.

The main point here is that, while theme-based investing is undoubtedly a good way to make money, one must first of all have the ability to spot a theme first that is likely to give good returns over a long period of time and then choose the right stocks that will benefit from this. If not, then relying on a good fund manager or research house would be the appropriate thing to do.

Thus, at the current juncture, the one good way to invest would be to invest in small quantities at pre-determined regular intervals in fundamentally sound stocks with some value still left in them. We know that investment ideas at the current levels are difficult to come by, but a little bit of hard work and extra research could help you recognise a few of them. This type of investing pattern would not only help an investor to be a part of the rally (if it continues), it would also protect him/her from over-exposing to equities at the current historic high levels and would thus protect him/her from getting severely hurt in the case of a correction. Moreover, even if a correction comes by, the investor would not have to worry on account of his fundamentally safe investments. Happy and safe investing!

Where is investing guru Mark Mobius looking next? President of Templeton-Emerging Markets, Mark Mobius is regarded as the Indiana Jones of the industry. His home is a hotel room, he commutes by jet, his religion is his work. When Mobius talks, people usually listen in pindrop silence. Click here for the whole interview.

by David McEvan

"The investor with a portfolio of sound stocks should expect their prices to fluctuate and should neither be concerned by sizeable declines nor become excited by sizeable advances. He should always remember that market quotations are there for his convenience, either to be taken advantage of or to be ignored. He should never buy a stock because it has gone up or sell one because it has gone down. He would not be far wrong if this motto read more simply: Never buy a stock immediately after a substantial rise or sell one immediately after a substantial drop."

This is easy to forget. Unless you need to sell shares to raise cash in the next few weeks, it is not relevant what their price is. Far more important is the financial strength and management quality of the company. A good company will always survive and sometimes even prosper during the inevitable ups and downs of the economy.

Those who do not need to raise cash in the short term should keep in mind the good times that will inevitably return, while taking solace in the dividends good companies churn out year after year. Here is a passage from another book, The Warren Buffett Portfolio, by Robert Hagstrom.

"If we were to ask Buffett what he considers an ideal holding period, he would answer, `Forever' – so long as the company continues to generate above-average economics and management allocates the earnings of the company in a rational manner.

" `Inactivity strikes us as intelligent behaviour,' he explains. `Neither we nor most business managers would dream of feverishly trading highly profitable subsidiaries because a small move in the Federal Reserve's discount rate was predicted or because some Wall Street pundit has reversed his views on the market.' Why, then, should we behave differently with our minority positions in wonderful businesses?"

That is a key point – good investors buy businesses, not shares. All businesses have very profitable years and not so profitable years. The key number to the long-term investor is the return on their capital – shareholders' funds. If a company is generating a return that is better than other investment options such as cash, bonds or property then the investor should be happy to let the money sit there and grow.

Return on capital has nothing to do with the share price on any given day. Instead, it is a measure of how much is earned and poured back into the business – the real formula for success that share prices often fail to depict. It is measured by taking net profit as reported, and dividing that by shareholders' funds as shown in the balance sheet. Buffett has said if that ratio ends up being 15 per cent or higher, you have a real growth investment.

The share price is not that important. Your target should be to find good companies with reliable earnings that generate a return on equity of 15 per cent or more – without the weak balance sheet that can distort that number.

Click on the link to read the full story

"Investors were irrationally exuberant during the bubble years of 2000. And that's exactly why the shrewd market players today should be feeling confident. Look at it this way, "Six years ago we could do no wrong, and everything was possible in the world. Today everything seems exceedingly challenging. We were wrong six years ago. And I think we could very well be wrong today." In Stock Market, it most often pays not to follow the leader. No one wants to hear that. It's almost irresistible to believe that after all we investors have endured -- the hellish bear market, the recession, the scandals -- we've emerged from the crucible sadder but wiser, finally willing to face the truth about stock values. But it isn't so. The amazing reality is that we haven't learned our lesson even yet."

Click on the link to read the full story

Indian organised retail to triple by 2010 - report

Foreigners own 30% of India Inc

Soaring input costs hang heavy on battery stocks underperform Sensex

The Compass: Wipro: A Logical move & Steel Prices

Analysts` corner: Petronet LNG

Stock watch: MTNL

All investors are Liars by John Allen Paulow

One pound of learning requires ten pounds of common sense to apply it.

In case of a crash or emergency, be it the stockmarkets or the road, how fast will the stock go down, and in case of a car, the buyer is not interested in knowing how much time will it take for his vehicle to come to a standstill, basically from 60 to 0 km/h.

One can also relate the stock markets to a traffic signal on the road. Aware as everyone is, there are 3 lights - red, yellow and green. In mid-2003, the markets were in the green mode, as we were entering the bull phase and if an investor put his hand in any stock, he soon realised that it doubled within a year. Then, as the markets gained momentum and reached new highs, we entered the yellow signal, wherein investors only with a high risk appetite could invest, as the upside seemed way less then the downside risk, and a similar situation happens on the road, as drivers who are cautious stop with the yellow light, while less cautious ones jump the signal, indicating their risk-taking ability (in case of cars, facing the cop). However, when the signal turns red, its time for everyone to stop, like in the stock markets, when they are overheated, its at least time for retail investors to take the back seat.

We had recently conducted a poll on our website, asking our viewers, that in the current bull run, in which segment had they made money, was it large, mid or small cap. The outcome was quite stiff - 50% said that they made money in small cap stocks, 24% made money in mid-cap, while the rest made in large cap stocks. With this outcome, we are sure that the passion for mid and small cap stocks amongst investors is not yet over and that they yet see potential in them.

Even we agree that opportunities exist everywhere, at every level for large cap stocks and even for select, fundamentally strong mid-cap stocks. But if one takes the trouble to go back in history, mid-cap stocks have been the first ones to be gunned down in case of any correction. But, as we wrote in the first paragraph of this article, people do not bother to check how fast is the downward run going to be in case of an event or correction.

Thus in conclusion, we do not say who is right or wrong, but ultimately, everything melts down to justifying valuations. Today, an institution might be ready to give a stock a P/E multiple of 20x its forward earnings, while a retail investor will be comfortable only with 15x its earnings going forward for the same period. Who in this case should we say is right? The thumb rule says that if a company's profits are growing at 15% YoY for a consistent period, it can be given a P/E multiple of 15x and if 20% then 20x and so on and so forth. However, one must keep in mind that there are other factors, like economy scenario, sector outlook and so on that also need to be clubbed in while projecting, and then arriving at a suitable valuation.

Experts and Markets

Overall, the evidence suggests there is little benefit to expertise . . . Surprisingly, I could find no studies that showed an important advantage for expertise. - J. Scott Armstrong, The Seer-Sucker Theory: The Value of Experts in Forecasting

Given that the stock market is a probabilistic, high-degree-of-freedom domain and the poor aggregate performance of active investment managers, there seems little reason to look for investing experts. However, a handful of distinguished investors have established excellent long-term records, which holds hope for expertise in investing.Economist Burt Malkiel says it this way:

While it is abundantly clear that the pros do not consistently beat the averages, I must admit that there are exceptions to the rule of the efficient market. Well, a few. While the preponderance of statistical evidence supports the view that market efficiency is high, some gremlins are lurking about that harry the efficient-market theory and make it impossible for anyone to state that the theory is conclusively demonstrated.

Since we don’t yet understand all the issues around expertise and have yet to study successful investors in great detail, our conclusion that there are expert investors is tentative. However, it does not appear expert-investor skill sets are transferable.

Here are some of the characteristics expert investors share:

• Successful investors put in plenty of deliberate practice.

In investing, this generally means lots of time reading, often across diverse fields. For example, the highly-regarded head of GEICO’s

investments, Lou Simpson, says, “I’d say I try to read at least five to eight hours per day. I read a lot of different things . . .” Berkshire Hathaway’s Charlie Munger makes the point more emphatically, “In my whole life, I have known no wise people (over a broad subject matter area) who didn't read all the time—none, zero. You'd be amazed at how much

• Great investors conceptualize problems differently than other investors.

As a group, these experts go beyond the near-term obvious issues, can identify relevant principles because of their experience, and see meaningful trends. These investors don’t succeed by accessing better information; they succeed by using the information differently than others. As an illustration, star investor and Sears Holdings chairman Eddie Lampert carefully studied Warren Buffett’s past investments to understand the logic. By reading annual reports in years preceding Buffett deals, Lampert sought to reverse engineer Buffett’s thought process. In a Business Week article, Lampert noted, "Putting myself in his shoes at that time, could I understand why he made the investments? That was part of my learning process."

• Long-term investment success requires mental flexibility.

Just as markets constantly evolve, so too must investors. Further, expert investors possess the second type of flexibility—an ability to

recognize when their easily-accessible mental models no longer apply. This recognition requires a return to basic principles to think carefully about a topic.

Bill Miller’s investment-process evolution is a good case:

The [conventional value investing] approach that had been so successful for us . . . had serious shortcomings when the economy peaked and began to head down. I decided to see if the academic literature offered any insights into how we might improve our investment process. After reviewing the data . . . it became clear that the conventional wisdom about value investing was wrong. Our experience in the late 1980’s and the changes we implemented in our process allowed us to sidestep that [performance] pothole in the late 1990s.

• Not pattern recognition but process recognition.

As scientist Norman Johnson notes, in complex systems an expert can create a mental simulation, fueled by diverse information. An idea or

problem solution emerges from the simulation, leaving the expert unable to explain how he or she arrived at the solution. 23 A colleague’s description of legendary hedge fund manager George

Soros makes this point:

[

The research on expertise is ambiguous on how much of expertise we can attribute to innate characteristics versus deliberate practice. For example, Ericsson and Smith report, “the research approach of accounting for outstanding and superior performance in terms of general inherited characteristics has largely been unsuccessful in identifying strong and replicable relations.” 25 Our view, in contrast, is there is clearly a hard-wired element to investing success. That most investors with outstanding long-term records share a similar personality profile supports this view.

Summary

Some skepticism about the value of experts is clearly warranted. An expert’s ability to solve a problem appears largely dependent on the problem type. Computers tend to solve simple problems better, and cheaper, than experts, while collectives outperform experts for complex problems.

Click on the link to read the full story Beware Of Too Much Diversification 'Herd mentality of FIIs can destabilise markets'

Shimmering metal(Aluminium) & Thomas Cook

{kind=link}