Markets: Irrational exuberance

Source: DNA Money

Despite warnings from leading brokerages that most Indian stocks are expensive, the Sensex continues on its northward journey. Optimists who defend the rally say that the price-earnings valuation of the Sensex is only about 20 times currently, much lower than the peak valuations in earlier rallies. That may be true, but it also needs to be noted that the PE of the Sensex is pulled down by oil and metal stocks, which trade between 7 and 14 times trailing earnings. Excluding these stocks, the Sensex PE shoots up to 26 times.

But what’s wrong with a high PE, one may ask, if earnings growth is going to keep pace? For instance, if a company trades at a PE of 30 times (stock price of Rs 300 and earnings per share of Rs 10) and its earnings are expected to grow at 30%, it’s said to have a fair valuation. In this case, the company has a price-earnings/growth (PEG) ratio of 1, and a PEG of 1 or below normally means that the valuation is not high. The problem with the PEG ratio, however, is that it normally takes a short-term view of earnings growth estimates. Most times, earnings estimates are available only for the next two years, and these figures are used while calculating the PEG ratio.

What would be much more useful to know is how long earnings of the company need to grow by 30% to justify a PE of 30 times. It turns out that profit would have to grow by 30% for at least 9 years to justify a PE of 30 times. This calculation is based on the assumption that the company maintains its dividend payout at 25% of profit (in order to get an incremental return on equity of 40%) for the first 10 years. Beyond the 10th year, earnings growth is assumed to be 6%, in line with the expected growth in nominal GDP 10 years hence, and dividend payout is expected to increase to 88% (again, in order to get an incremental return on equity of 40%). The dividend receipts arrived at till perpetuity, when discounted assuming a cost of equity of 14%, gives a present value of Rs 332 if growth is taken at 30% for the first 10 years, slightly higher than the stock price of Rs 300. If the period for which growth in earnings is expected to be 30% is cut to nine years, the present value comes to Rs 286 (with other assumptions such as ROE remaining the same).

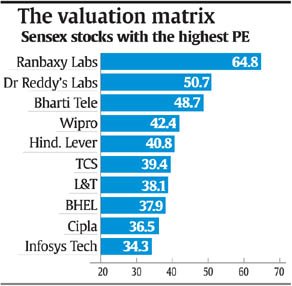

The crux of all this is that a company which currently trades at a PE of 30 times and maintains a dividend payout of about 25%, must grow earnings by 30% for the next nine years. In other words, not only are the markets building in high growth expectations into stock prices, but earnings growth is being estimated at high levels for long period of time. The table alongside shows the Sensex stocks that currently have a price-earnings ratio of 30 times. Analysts point out that for some stocks like Wipro and TCS, earnings must grow by 25% each year for at least the next 16 years, in order to justify current valuations. It needs to be noted, finally, that the above calculation gives only a broad sense of earnings expectations being built in. In the case of specific companies, different results could throw up, depending on the ROE of the particular company and assumptions on dividend payout.

The strangest thing is - it is these smae stocks .. with a higher P/E which are going up... while stocks on a lower P/E even single digit PE are sagging.

Warm Rgds

Shankar

Posted by Shankar Nath |

2:47 PM

Shankar Nath |

2:47 PM